How RIAs Can Bring Real Asset Precision to Modern Portfolio Construction

In the face of stubborn inflation and an increasingly volatile market, many advisors are rethinking the building blocks of portfolio design. Real assets, once a fringe allocation, are now gaining traction as practical tools for diversification and volatility management.

Among these, agricultural commodities are drawing increasing attention. However, with the growth of agriculture-themed ETFs, a new challenge has emerged: not whether to allocate, but how to select the right vehicle for each client’s needs.

This article outlines a framework that RIAs may use to evaluate agricultural ETFs, helping them make informed, real-world, portfolio-driven decisions with confidence.

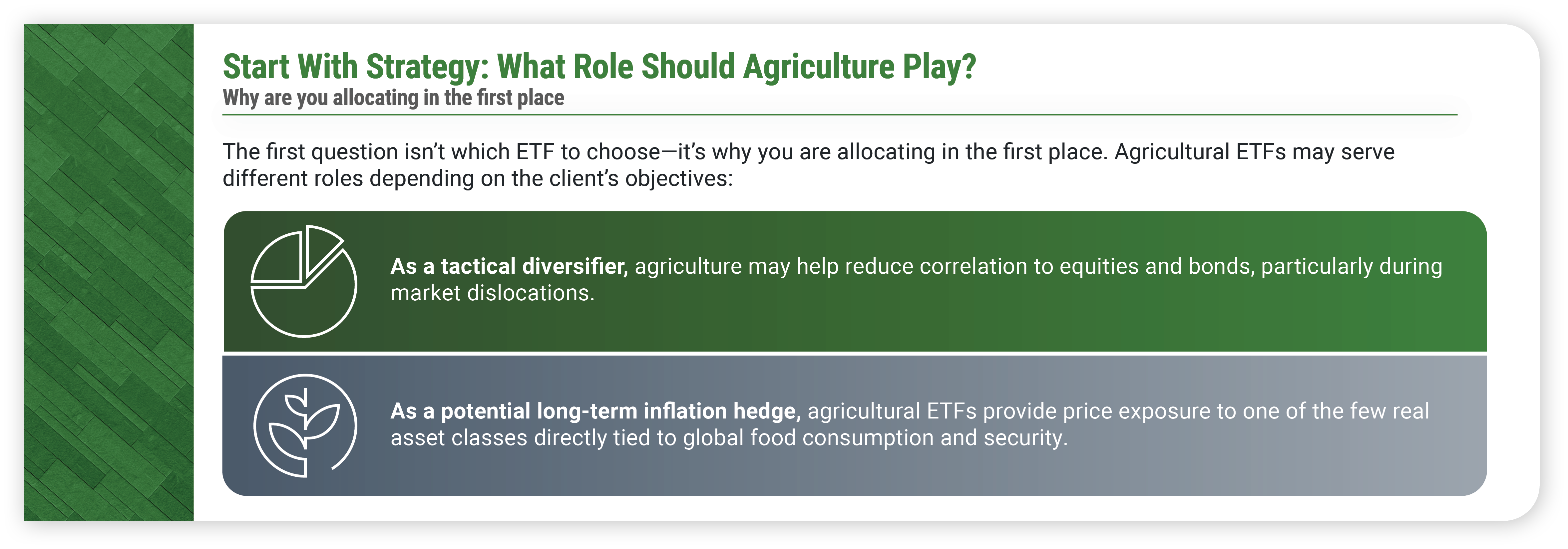

Start With Strategy: What Role Should Agriculture Play?

The first question isn’t which ETF to choose—it’s why you are allocating in the first place. Agricultural ETFs may serve different roles depending on the client’s objectives:

-

As a tactical diversifier, agriculture may help reduce correlation to equities and bonds, particularly during market dislocations.

-

As a potential long-term inflation hedge, agricultural ETFs provide price exposure to one of the few real asset classes directly tied to global food consumption and security.

Understanding these roles also means understanding the realities of commodity volatility. Agricultural prices can be seasonally and geopolitically sensitive. Position sizing and rebalancing policies should reflect an investor’s risk profile.

Know What’s Under the Hood: Single Commodity vs. Basket Strategies

Once the role is defined, the next step is to evaluate how each ETF delivers that exposure. Broad agricultural baskets may offer diversified access to multiple commodities, but may dilute the impact of any one market. Single-commodity ETFs, such as Teucrium’s CANE, CORN, WEAT, and SOYB, enable advisors to make more precise allocations based on macroeconomic themes or client-specific views.

Equally important is understanding how these ETFs obtain their exposure. Teucrium’s products use futures contracts, not equities or physical commodities, allowing for:

-

Direct futures price exposure to core U.S. crops

-

Holding multiple contracts across the futures curve, spreading price exposure to various contract dates.

-

Transparency that helps advisors clearly explain the strategy to clients

Don’t Overlook Liquidity, Tax, and Product Structure Considerations

Beyond strategy and structure, RIAs should carefully evaluate operational factors such as:

-

Regulatory Structure: Teucrium ETFs are registered under the Securities Act of 1933, not the Investment Company Act of 1940. This means they may have different operational characteristics than traditional ’40 Act funds.

-

Tax Reporting: Teucrium’s single commodity ETFs issue K-1 forms, not 1099’s which have unique and sometimes beneficial tax characteristics.

-

Liquidity and Scale: Advisors should understand that ETF liquidity is driven not only by the fund's assets under management but also by the depth of the underlying futures market and the ETF's unique creation and redemption mechanism. For example, as of June 25, 2025, the Teucrium WEAT ETF manages approximately $120 million in assets. However, between $2 and $4 billion worth of Chicago wheat futures trade daily—demonstrating the significant liquidity available in the underlying market.[1]

Moreover, as with all ETFs, when investor demand exceeds the current supply of shares, authorized participants can request the issuer to create additional shares. Conversely, when selling pressure dominates, shares can be redeemed, effectively removed from circulation. This create/redeem process helps ensure that ETF prices stay aligned with their underlying value and supports overall market liquidity.

These considerations might influence how you position the ETF with different client types, from retirees seeking simplicity to traders seeking tactical flexibility.

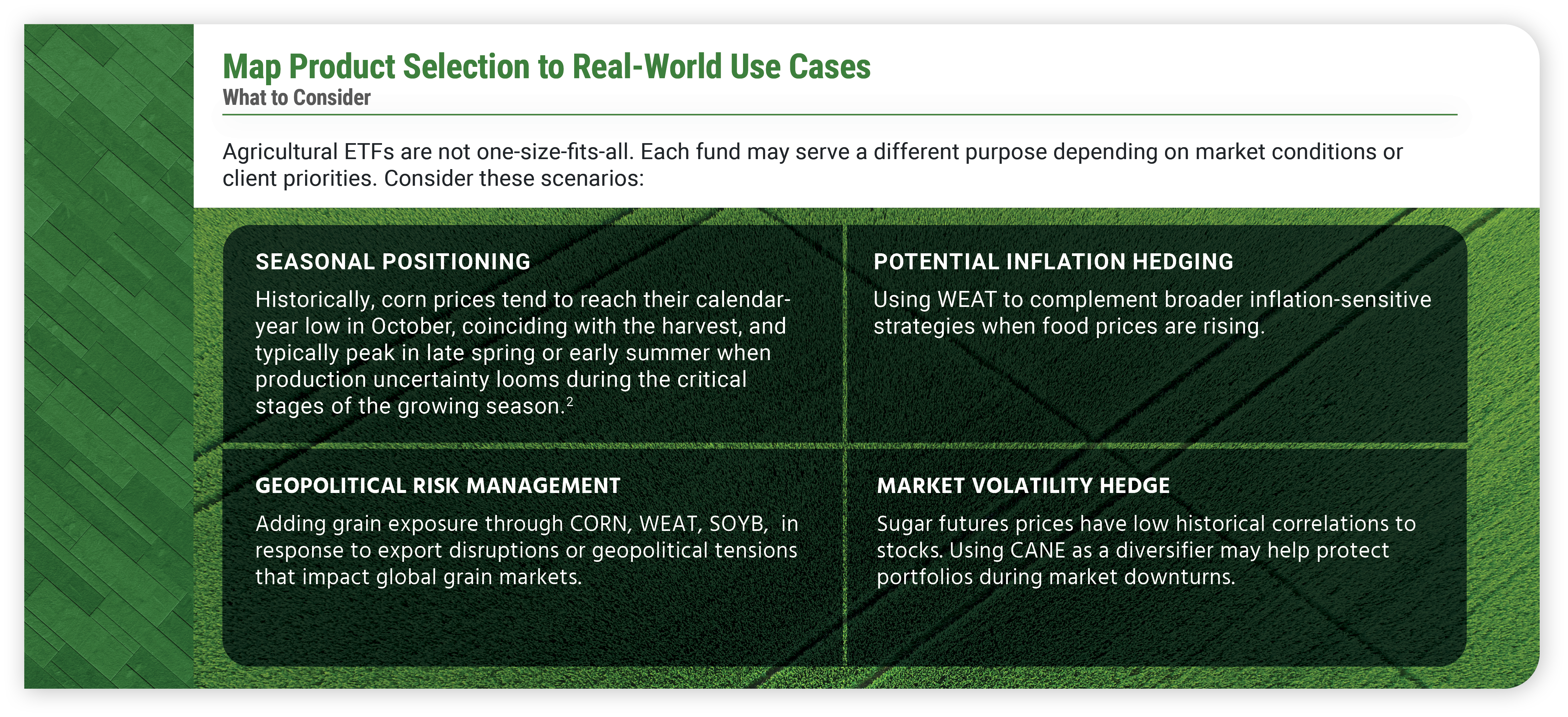

Map Product Selection to Real-World Use Cases

Agricultural ETFs are not one-size-fits-all. Each fund may serve a different purpose depending on market conditions or client priorities. Consider these scenarios:

-

Seasonal Positioning: Historically, corn prices tend to reach their calendar-year low in October, coinciding with the harvest, and typically peak in late spring or early summer when production uncertainty looms during the critical stages of the growing season.[2]

-

Potential Inflation Hedging: Using WEAT to complement broader inflation-sensitive strategies when food prices are rising.

-

Geopolitical Risk Management: Adding grain exposure through CORN, WEAT, SOYB, in response to export disruptions or geopolitical tensions that impact global grain markets.

-

Market Volatility Hedge: Sugar futures prices have low historical correlations to stocks. Using CANE as a diversifier may help protect portfolios during market downturns.

You might position a growth-oriented client with a tactical tilt toward a single commodity ETF, while suggesting a conservative income client start with a small, diversified allocation to test fit and comfort.

Start the Client Conversation Now

Agricultural ETFs may not dominate portfolio headlines, but their role as real asset diversifiers is gaining relevance. Rising food demand, geopolitical instability, and inflationary pressures all point to the timeliness of this conversation.

Starting small, perhaps with a single commodity ETF, may open the door to broader client discussions about real assets, volatility management, and portfolio resilience.

Explore how Teucrium’s ETFs can fit into your client portfolios. Schedule a meeting with an investment strategist here.

Footnotes for Blog:

[1] CME Group. "CME Group to Add Spring Wheat Futures Contract." Northern Ag Network, January2025.https://www.northernag.net/cme-group-to-add-spring-wheat-futures-contract/.northernag.net

[2]Bryce Knorr, "Profit Opportunities in Seasonal Price Patterns," Farm Progress, February 15, 2018, https://www.farmprogress.com/commentary/profit-opps-in-seasonal-price-patterns

Important Disclosures and Risk

The information provided is intended to provide a broad overview for discussion purposes. It is subject to change and should not be taken as financial, tax or investment advice. Teucrium Trading, LLC and Teucrium Investment Advisors, LLC make no offers to sell, solicitations to buy, or recommendations for any security, nor do they offer advisory services.

This material must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing. To obtain a current prospectus visit:

Teucrium Corn Fund (CORN): CORN | Teucrium

Teucrium Soybean Fund (SOYB): SOYB | Teucrium

Teucrium Wheat Fund (WEAT): WEAT | Teucrium

The Teucrium Sugar Fund (CANE): CANE | Teucrium

CORN, CANE, SOYB and WEAT are commodity pools regulated by the Commodity Futures Trading Commission (CFTC). These Funds, which are ETPs, are not mutual funds or any other type of Investment Company within the meaning of the Investment Company Act of 1940, as amended, and are not subject to regulation thereunder. The funds do not track the spot price of corn, sugar, soybeans or wheat.

Commodities and futures generally are volatile and are not suitable for all investors.

Futures investing is highly speculative and involves a high degree of risk. An investor may lose all or substantially all of an investment. Investing in commodity interests subject each Fund to the risks of its related industry. These risks could result in large fluctuations in the price of a particular Fund's respective shares. Funds that focus on a single sector generally experience greater volatility. Futures may be affected by Backwardation: a market condition in which a futures price is lower in the distant delivery months than in the near delivery months. As a result, the fund may benefit because it would be selling more expensive contracts and buying less expensive ones on an ongoing basis; Contango: A condition in which distant delivery prices for futures exceed spot prices, often due to costs of storing and inuring the underlying commodity. Opposite of backwardation. As a result, the Fund’s total return may be lower than might otherwise be the case because it would be selling less expensive contracts and buying more expensive one. For further discussion of these and additional risks associated with an investment in the Funds please read the respective Fund Prospectus before investing.

Diversification does not ensure a profit or protect against loss.

Teucrium Trading, LLC is the Sponsor for CORN, CANE, SOYB, and WEAT. PINE Distributors LLC is the Marketing Agent for CORN, CANE, SOYB, and WEAT, and is not affiliated with Teucrium Investment Advisors, LLC and Teucrium Trading, LLC.

Past performance is not indicative of future results. Teucrium disclaims any liability for any actions taken based on the information provided in this document.

TUCRM-4613306-6/25

Topics:

{kind=link}