Energy Market Views from the Desk of Sal Gilbertie

Front-month Brent traded near $97 a barrel this week, up roughly 66% since the start of the year.[1] The move occurred against the backdrop of a historic supply shock out of the Strait of Hormuz, where roughly a fifth of the world's seaborne oil moves.[2] In our view, that move has now re-priced crude to fair value.

The disruption is still severe, but the physical market has settled into a fragile equilibrium.

High prices did their job.

Real demand destruction is now balancing the barrels the war took offline. The headline supply numbers still read as a crisis, but the trading data tells the other half of the story.

High prices did the work.

Vitol pegs global demand destruction at roughly 4 million barrels per day.[3] Tom Baker, who runs Vitol's Bahrain desk, told a London conference this week that the spikes in gasoline, diesel and jet fuel prices have crushed consumption across developing Asia and parts of Africa. The IEA tells the same story from the top down. It now sees world oil demand contracting by 420,000 barrels per day in 2026, to 104 million, 1.3 million below its pre-war forecast, with the second quarter taking the deepest hit as aviation and petrochemicals pull back.[4]

Supply fell further than demand, so the market is genuinely short. The IEA puts the 2026 deficit at 1.78 million barrels per day and sees total supply down 3.9 million on the year as Gulf OPEC+ output collapses.[5] But that gap is far smaller than the raw supply loss alone would imply, because price did the rationing.

Baker framed it the same way, calling demand destruction the only mechanism left to balance the market if the shortage drags on, though he stopped short of saying we have hit that point. That is what fair value looks like in a supply crisis: crude climbed until demand backed off enough to roughly clear the books.

China is the swing buyer.

China is the world's largest crude importer, has stepped back hard.[6]

Seaborne crude imports fell to about 6.36 million barrels per day in May, the lowest in nearly a decade, down from 8.10 million in April and 11.39 million back in February. That is a drop of roughly 5 million barrels per day in three months.[7]

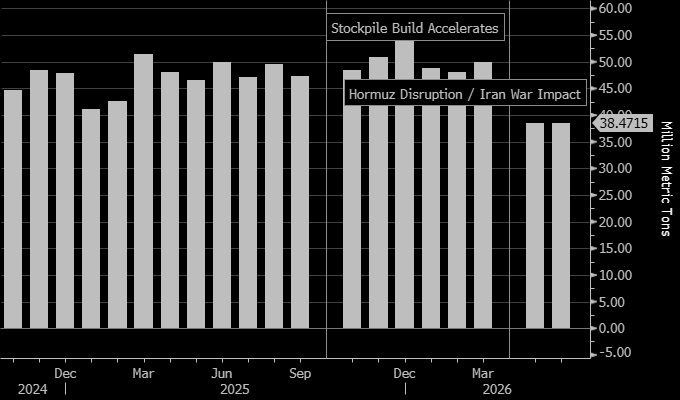

The Bloomberg chart below provides a monthly perspective for all Chinese crude imports. You can see that in April 2026 total imports collapsed ~20% year-on-year to 38.5M metric tons. That, is the lowest since July 2022.

Source: China General Administration of Customs via Bloomberg (CCCIIQTL INDEX); Bloomberg News.

China’s economy still needs oil, so this is not entirely a story about demand destruction and more about Chinese buyers seeking cheaper alternatives. China cut the expensive Brent-priced grades and has sought to covered the gap two ways.

- Drawing down strategic and commercial reserves.

- Sourcing heavily discounted Russian and Iranian crude wherever it could get it.

That combination seems to be helping meet Chinese energy demand for now, but the clock is ticking. Baker did not mince words: China “won't indefinitely not import 5 million bpd, and at some point when they need those barrels, the price needs to go higher.”[8]

We think a sudden return of Chinese buying is a primary upside risk from here. As long as global demand stays soft and Chinese imports stay depressed, in our view the market looks fully and fairly priced.

A re-escalation risk premium.

The fragile equilibrium we describe assumes the kinetic conflict stays contained. The other clear upside risk to prices is a re-escalation of the fighting.

A renewed flare-up around the Strait would not need to take fresh barrels offline to move the market. The threat alone tends to do the work, as traders rebuild a risk premium into the price to compensate for the chance of a deeper or more lasting disruption. A market that has settled near fair value on the assumption of an uneasy truce would have to price the renewed possibility of prolonged war. That presents another clear upside risk for prices.

Hormuz and the hidden barrels.

Set against those upside risks, the clearest downside risk is the strait reopening. Tanker traffic through Hormuz fell roughly 70% once the conflict began, war-risk insurers pulled cover, and well over a hundred ships anchored outside the chokepoint to wait it out.[9] A return to normal flows would loosen the squeeze quickly, and we think that could pull prices lower.

Even now, however, there are reports of some ships getting through the Strait. Crude-laden tankers are going dark, switching off their transponders to move through the region undetected. In a single week in May, three supertankers slipped out of the strait with trackers off, carrying roughly 6 million barrels between them.[10]

The dark-sailing vessels spanned multiple flags, owners and cargo origins, so this appears to be mainstream commercial operators adopting the tactic, not just the usual shadow fleet. We think that suggests actual outflows could already be running higher than the official tracking shows. Every barrel that gets through eases the physical squeeze and helps to ease upward pressure on prices.

What it means for market participants

The year-to-date run has done its job. We see the risks as roughly balanced from here and view crude as fairly valued at current levels.

The directional edge here is thin while the tails are fat on both sides. A snap-back in Chinese buying or a re-escalation of the fighting could shock prices higher. A Hormuz reopening layered on top of underreported flows could pull them down. That is a market where realized volatility can stay elevated even when the directional call is a wash, so the convexity deserves more attention than the heading.

Sizing a position on a flat directional view here, we believe, understates the risk in the tails. The three triggers to watch are a restart of Chinese imports, a re-escalation of the fighting, and the reopening of the strait. Until one of them breaks, we read crude as fairly valued.

Neutral, for now.

Notes

1. “Current Price of Oil as of June 2, 2026,” Fortune, June 2, 2026, https://fortune.com/article/price-of-oil-06-02-2026/.

2. “Strait of Hormuz Disruption Sends Oil Prices Surging,” World Bank Blogs, 2026, https://blogs.worldbank.org/en/opendata/strait-of-hormuz-disruption-sends-oil-prices-surging.

3. “Vitol Executive Warns West Is ‘Asleep at the Wheel’ on Oil Supply Crisis,” World Oil, June 2, 2026, https://worldoil.com/news/2026/6/2/vitol-executive-warns-west-is-asleep-at-the-wheel-on-oil-supply-crisis/.

4. International Energy Agency, “Oil Market Report – May 2026” (Paris: IEA, May 13, 2026), https://www.iea.org/reports/oil-market-report-may-2026.

5. IEA, “Oil Market Report – May 2026,” May 2026.

6. U.S. Energy Information Administration, “China, the United States, and Japan Hold Most Strategic Oil Inventories in 2025,” 2025, https://www.eia.gov/todayinenergy/detail.php?id=67504.

7. “China's Crude Import Decline Driven by Market Forces, Not Generosity,” ChemAnalyst, 2026, https://www.chemanalyst.com/NewsAndDeals/NewsDetails/chinas-crude-import-decline-driven-by-market-forces-42535.

8. World Oil, “Vitol Executive Warns West Is ‘Asleep at the Wheel,’” June 2, 2026.

9. “Hormuz Tankers Going Dark: Trackers Switched Off in 2026,” Discovery Alert, May 2026, https://discoveryalert.com.au/strait-hormuz-oil-flows-ais-dark-tankers-2026/.

10. Discovery Alert, “Hormuz Tankers Going Dark,” May 2026.

{kind=link}