The North American planting season is on the horizon, and the U.S. is gearing up to sow what could be a game-changer for corn and soybean markets in 2025-2026. Fresh off the USDA's 101st Agricultural Outlook Forum today, the numbers are in, and they're pointing to a bumper crop for corn and a steady, if uncertain, ride for soybeans.

Corn's Big Haul

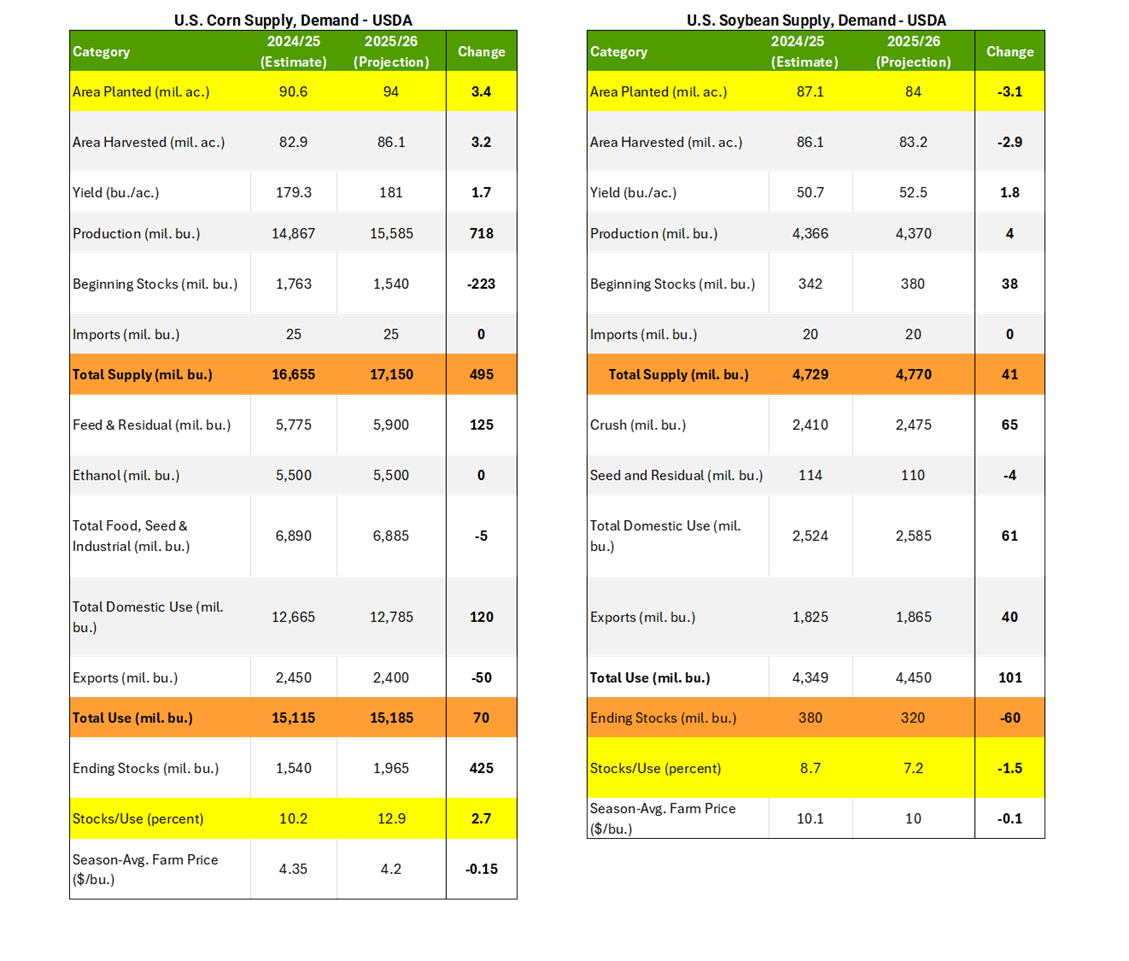

The U.S. corn balance sheet is projected to expand in the '25-'26 marketing year. The expansion would largely be driven by a 3.4 million-acre jump in plantings versus last year. As the USDA sees it, we should expect 94 million corn acres planted with an average yield of 181 bushels per acre. That's enough to push production to 15.585 billion bushels. Based on current demand projections, the result is a 425 million bushel increase to ending stocks and a stocks/use ratio of 12.9%.

The domestic figures will work into a global balance sheet that has been contracting for the past two years. While the global corn balance sheet is nowhere near as flush as the soybeans (see below), there is still plenty of corn in the world.

Fundamentally, an expanding balance sheet is a recipe for lower prices. As we approach the planting season, we anticipate downward pressure on prices, barring any unexpected surge in demand. Of course, the weather is always a wildcard.

Soybeans: Steady with a Twist

The U.S. soybean balance sheet may tighten slightly in '25-'26. Current expectations are for plantings of 84 million acres, a year-over-year decline of 2 million acres. Given reduced acreage, soybean farmers face the challenge of achieving substantial yields to maintain adequate ending stocks. USDA projections are for a 52.5 bushel per acre (bpa) yield well above the 50.7 bpa yield in '24-'25 and a 50.6 bpa yield in '23-'24. A national average yield of 52.5 would bring production up to 4.37 billion bushels, which, based on current demand projections, would result in a 50-million-bushel year-over-year reduction in ending stocks.

Still, even if supplies tighten in the U.S, the global balance sheet remains flush. The global stocks/use ratio approached record highs in the current marketing year. There are plenty of soybeans in the world, and we expect it would take a significant supply or demand surprise to tip the scales in favor of the bulls.

Prices in the Crosshairs

The outlook for corn futures is a bit bearish as we approach planting season. With higher stocks and increased acreage on the horizon, we're likely to see some downward pressure on prices. We would not be surprised if we dip below the $4 mark unless global demand suddenly surges.

Soybeans, on the other hand, are keeping us on our toes. With the potential for a tightening U.S. balance sheet, prices might hover around $10, but be prepared for some wild swings, particularly if the global balance sheet continues to expand. We'll be watching weather conditions, the efficiency of planting operations, and the yield outcomes from South American harvests.

As we approach the Spring planting season, market participants should remain vigilant, as this period typically brings heightened volatility and potential opportunities.

Topics:

{kind=link}