This was a week where market participants came in pricing for headlines and got them in full force.

The U.S.-China summit in Beijing wrapped without new explicit agricultural purchase agreements, the May WASDE put U.S. winter wheat production down roughly 25% year-over-year, and India’s government slammed the door on sugar exports through September 30.

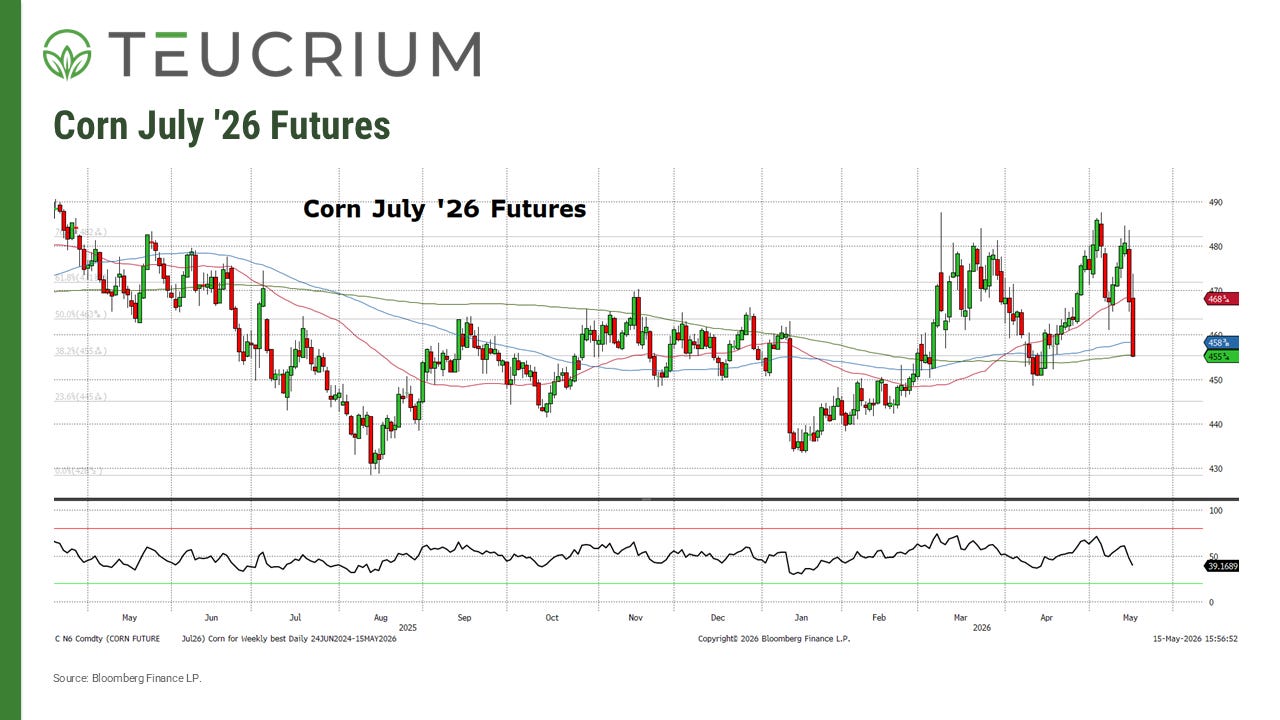

Corn

CBOT corn front-month settled at 455.25¢/bu Friday, after touching a weekly high of 467.25¢/bu Monday. The dominant theme was the Beijing summit, which closed without fresh export commitments. Friday’s session saw corn fall 2.4% to 2.5% as improving U.S. weather added to the bearish tone.

The CFTC positioning told the same story. Money managers cut net-long corn positions by 44,442 contracts to 299,483 for the week ending May 12, with short-only positions hitting a three-week high. That looks like funds de-risking ahead of summit headlines.

On the supply side, the global picture firmed up. Brazil’s CONAB raised its 2025/26 grain production forecast to a record 358 million tons, up from 356.3 million tons. Russia’s corn exports reportedly rose 1.6x year-over-year, and export duties on Russian corn are set to remain in place from May 20. Plenty of corn, weak demand catalyst, profit-taking on a long book. The tape behaved accordingly.

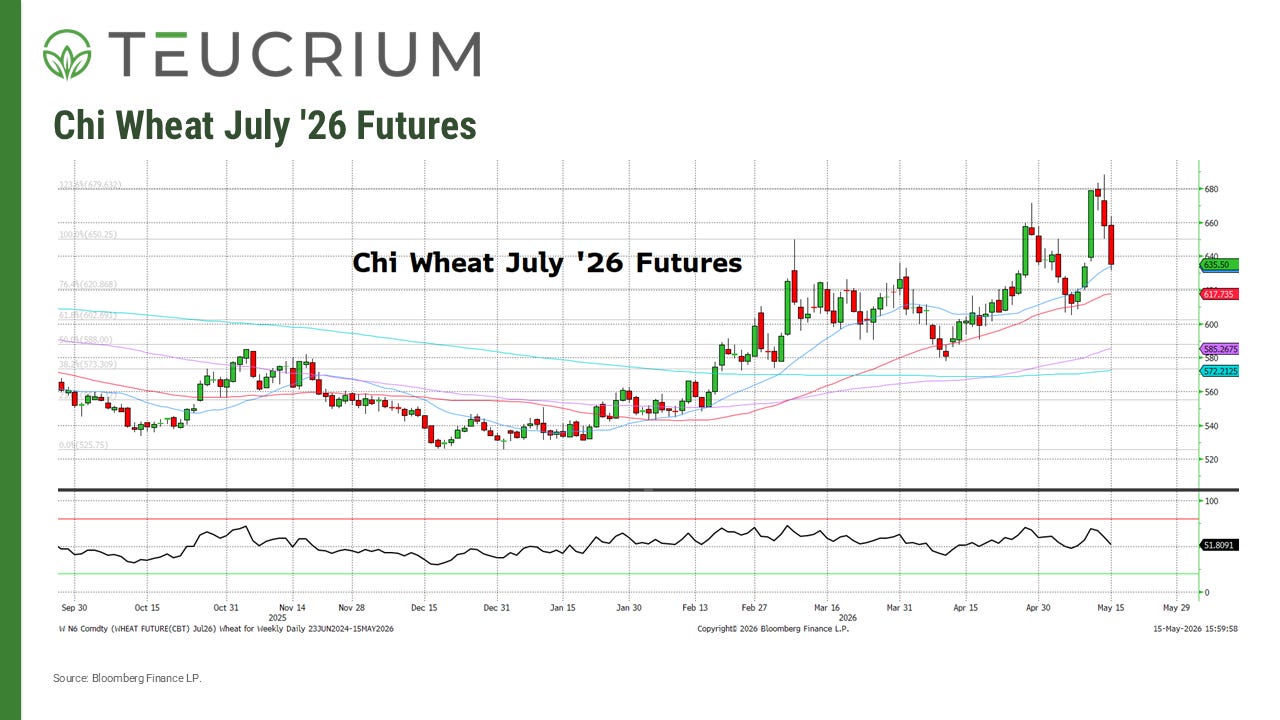

Wheat

Chicago wheat was the most volatile grain of the week. The May WASDE on Tuesday projected U.S. winter wheat production down roughly 25% year-over-year, sending futures up as much as 7.1% on May 12 to the highest levels in roughly two years. A crop tour confirmed drought, frost damage, and disease, with Kansas wheat yields projected at a three-year low. Hard red winter wheat hit its highest level since 2023 mid-week.

Then the tape reversed.

By Friday, September wheat had fallen 3.3% to $6.49½/bu as U.S. growing-area weather improved and the China summit failed to deliver new export deals. CFTC data showed money managers boosted net-bearish Chicago wheat bets by 9,120 contracts to 19,023, the most bearish positioning in more than two months, with short-only positions at a 10-week high.

A 25% production cut at the WASDE level is not a small number. Russia’s spring wheat planting is reportedly running at less than half the pace of a year ago, weighed down by heavy rains and cold weather. France’s Rouen port grain exports jumped 63% in the week to May 13, totaling 230,385 tons. In our view, the round-trip in the tape reads as fund repositioning around the summit. The supply backdrop did not improve.

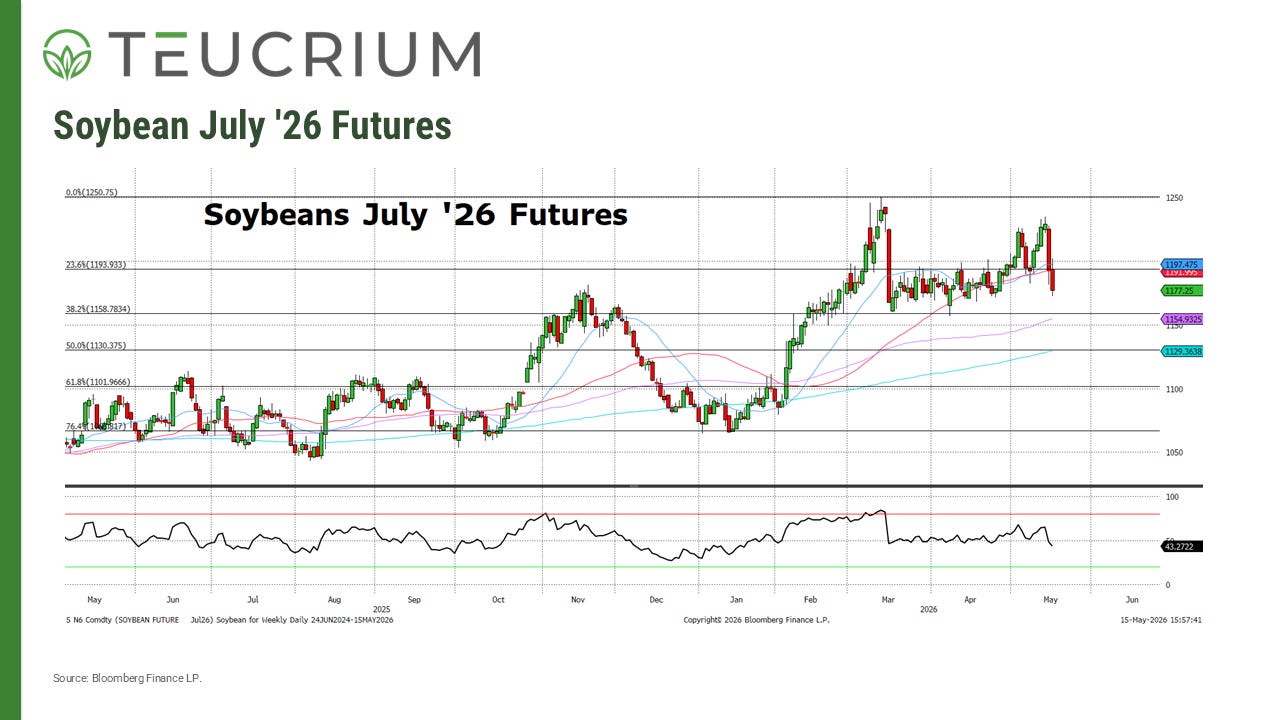

Soybeans

Soybeans held steady early in the week as traders awaited the Trump-Xi summit, with expectations that China would commit to purchases beyond the existing 25-million-ton annual pledge. Day one of the summit produced no new agricultural deals, sending August soybeans down 2.9% to $11.93¾/bu on May 14.

Friday became a study in mixed messages. President Trump stated that China “will buy billions of dollars of soybeans” and that a deal had been reached, but provided no specifics. U.S. Trade Representative Greer indicated expectations of “double-digit billion” in annual agricultural purchases over three years. Treasury Secretary Bessent then signaled that soybean commitments are “already taken care of” under the existing Busan agreement. Futures fell to a three-week low, with August soybeans settling at $11.76¼/bu, down 1.1% on Friday.

The April NOPA crush came in at 211.9 million bushels, below the Bloomberg survey of 215.8 million bushels, though above year-ago levels. Traders treated it as broadly neutral. A flash sale of 155,000 metric tons of soybean meal to Italy and Brazil’s record harvest revision rounded out the supportive-to-neutral data points.

The market wanted new firm commitments from Beijing and got rhetoric instead. We think the tape could remain choppy until the agricultural purchase language firms up into actual sales and/or firm commitments.

Sugar

Raw sugar (ICE No. 11) ended the week near 14.80¢/lb, retreating from a mid-week high of 15.38¢/lb on May 13. The headline event was India’s ban on sugar exports, effective immediately through September 30, covering raw, white, and refined sugar, as the government moved to protect domestic supplies amid lower output estimates. India’s gross sugar production for the current season is forecast at 32 million tons, down from an earlier 32.4-million-ton projection.

The week also coincided with New York Sugar Week, where analyst views on the 2026-27 global balance diverged sharply. Datagro projected a 3.17-million-ton deficit, Citi forecast 1.3 million tons, StoneX 550,000 tons, while Covrig Analytics saw only a 380,000-ton surplus, down from a prior 800,000-ton estimate. Hedgepoint projected Brazil’s Center-South sugar output at 39.9 million tons in 2026-27, with 47.5% of the cane crop directed to sugar.

The positioning data was contradictory in its own right. Hedge funds boosted net-bullish white sugar bets to a 12-week high, while CFTC data showed money managers increased net-bearish raw sugar bets by 5,701 contracts to 92,990. Freight costs are an additional concern, with Asian refiners locking in supply amid elevated shipping disruptions.

In our view, sugar has the cleanest setup of the four. The analyst community cannot agree whether 2026-27 prints a 3-million-ton deficit or a 380,000-ton surplus. That level of disagreement around a single growing season suggests realized volatility in sugar could stay elevated, regardless of which forecast proves most accurate.

Topics:

{kind=link}